Announcements

- SUNY College Essential Start Kit Program

- 2026-27 Loan Changes (OBBBA)

- Fall 2026 New Student Financial Aid Offers

- Fall 2026 NYS Excelsior Tuition Scholarship Application.

- Consent to Release Financial Aid & Billing Information

- Important Updates Regarding Summer Pell Grant Eligibility (current students only)

New SUNY College Essential Starter Kit

Starting your first year of college can be exciting, but the cost of setting up a

dorm room can create barriers to success, especially for students who have experienced

housing insecurity or homelessness. To help ensure that students begin their college

journey with the essentials they need, the SUNY College Essential Starter Kit Program provides eligible students who are attending a SUNY university with essential dorm-room

items. These items could include XL twin sheet sets, comforter, shower caddy, and

other college necessities.

Eligibility:

Students must be attending SUNY Delhi for the upcoming Fall 2026 school year and be

planning to live on campus.

In addition, students must

• have faced housing insecurity or homelessness in the 25-26 school year OR

• have been referred by high school McKinney Vento liaison or Foster care liaison

How to sign-up:

Fill out the College Essential Starter Kit form form by July 25th to apply for this benefit.

New 2026-27 Loan Changes from the One Big Beautiful Bill Act (OBBBA)

The One Big Beautiful Bill Act (OBBBA) includes significant changes to federal student loans, borrowing limits, and repayment options. The information below is subject to change.

Summary of changes:

- Loan reductions for part-time enrollment or when dropping a course

- Parent PLUS loan capped (new annual and lifetime limits)

- New graduate student loan limits (new aggregate and lifetime limits)

- New repaymant plans (and elimination of PSLF for new PLUS loans)

- Deferment options reduced

Resources:

- Follow updates from the Department of Education on their OBBBA Update webpage.

- Federal Student Aid Direct PLUS Loan for Parents

- New Parent Borrower Guide and the Current Parent Borrower Guide from the National Association of Financial Aid Professionals

-

Education Debt Consumer Assistance Program (EDCAP): FREE loan repayment, consolidation, forgiveness, default prevention, Parent PLUS Loan counseling, and more! EDCAP offers webinars, helpful resources, and one-on-one virtual sessions to NYS residents only. Contact EDCAP.

PART-TIME ENROLLMENT

Starting in 2026-27, federal regulations will require student loans to be reduced in direct proportion to their enrollment status when a student enrolls part-time or begins full-time and later drops/withdraws from a course. There is no legacy exception and this applies to all students, both graduate and undergraduate that borrow a subsidized and/or unsubsidized loan. Parent PLUS loans are excluded.

- What should students do if they need to drop or withdraw from a course?

-

Students who need to drop or withdraw from a course should talk to the One Stop Office for guidance, regardless of borrowing loans or not. The various financial aid programs have different requirements for maintaining eligibility.

- Am I eligible for a loan if I attend part-time?

-

Yes, however, the amount you can borrow in the subsidized and unsubsidized loan will change starting in 2026-27 based on the new Schedule of Reduction (SOR).

Students that enroll part-time or whose enrollment drops to part-time (from full-time), will need their loans reduced in accordance with changes to the law.

If a student begins part-time, their loan will be reduced in direct proportion to the annual full-time enrollment for their degree level.

- Can I make up credits to reach the annual full-time enrollment?

-

Yes, credits taken during the summer, fall, winter, and spring can be used towards full-time enrollment.

Students can also add late session courses such a B or K to make up additional credits. However, adding a late session course does not guarantee an increase or becoming eligible for other finanical aid.

Contact the One Stop Office before adding a course.

- Can I request to increase my student loan?

-

Students whose loan is based on a part-time enrollment status that later add additional credits can request to increase their loan. However, students cannot exceed the annual and aggregate borrowing limits.

To request a loan increase, follow the steps below:

-Log into the Student Forms portal at https://delhi.studentforms.com-Click on "Manage Requests"

-Open and submit the Loan Adjustment Request: Student Loans form

Note: Deadlines apply. Loans must be processed before the student stops attending, whether its the end of the semester/academic year, withdrawing from all coursework, or dropping below half-time.

- What actually happens if I drop a course and am no longer considered full-time?

-

When a student loan is adjusted and by how much will be based on the timing of dropping the course (if the loan was disbursed, what semester the drop occurred in, and how many credits the student remains enrolled in).

The Financial Aid Office will review all course drops/withdraws (at any point in the semester) to determine if student loans need to be reduced in the current term or if the future spring portion of the loan will need to be adjusted.

If a loan is reduced, this could create a balance due if the student was liable (or partially liable) for the course or it could reduce refund amounts. This is also true for students who initially enroll part-time, as their annual loan will be reduced to reflect their actual part-time enrollment before the loan disburses.

We encourage all students to register for courses early, complete all financial aid requirements early, and reach out to the One Stop Office if they plan to change their enrollment status.

- Example: Initial Part-Time Enrollment

-

Annual undergraduate full-time enrollment = 24 credits

A student enrolls part-time at 9 credits in the fall and plans to register for 9 credits in the spring. Based on their degree program and number of earned credits, their annual maximum Subsidized is $4,500 and Unsubsidized loan is $2,000.

18 annual credits / 24 annual full-time enrollment = 75% Schedule of Reduction (SOR)

Max Annual Sub Loan 4,500 * 75% = $3,375/year

Max Annual Unsub Loan 2,000 * 75% = $1,500/year

Graduate Program Example: More information will be provided at a later date.

Generally, a student's initial financial aid offer will include loan amounts based on a full-time status. Students thinking of enrolling part-time should contact the One Stop to have their loans adjusted.

- Example: Dropping from Full-time to Part-Time

-

Annual undergraduate full-time enrollment = 24 credits

A student enrolls full-time at 12 credits in the fall and plans to register for 12 credits in the spring. Based on their degree program and number of earned credits, their annual maximum Subsidized loan is $4,500 and Unsubsidized loan is $2,000.

After 5 weeks into the fall semester, the student dropped 3 credits. This changes their enrollment status to part-time at 9 credits.

21 annual credits / 24 annual full-time enrollment = 87.5% Schedule of Reduction (SOR)

Max Annual Sub Loan 4,500 * 87.5% = $3,937/year

Max Annual Unsub Loan 2,000 * 87.5% = $1,750/year

Impact: Since the course was dropped in the 6th week of courses, the student would receive a W grade and would be fully liable for the cost of the 3 credits. If their loan is reduced, it could create a balance due or a reduced refund amount.

Graduate Program Example: Information will be available at a later date regarding the full-time enrollment status but the same concept applies.

Generally, a student's initial financial aid offer will include loan amounts based on a full-time status. Students thinking of dropping or withdrawing from a course should contact the One Stop to review the implications.

PARENT PLUS AND GRADUATE UNSUBSIDIZED LOAN LIMITS

- What are the changes to loan limits starting in 2026-27?

-

Loan Type 2025-26 and prior

NEW 2026-27

based on OBBBATime Limited Legacy Exception: Parent PLUS Loan Amount Limits Annual Limit: Parent can borrow up to the student's annual Cost of Attendance (COA) minus other aid, annually.

Aggregate Limit: None

New Annual limit: $20,000 per dependent student

New Aggregate Limit: $65,000 (per student)

Annual & Aggregate Limit Exception: If a parent borrowed a Parent PLUS loan for a current student before July 1, 2026, they may be able to keep borrowing under the old rules for a short period of time. The length of this exception depends on the normal length of the student’s program (2, 4, or 5 years) and how long the student has already been enrolled in that program.

The exception can last up to 3 years, but it may be shorter if the program is shorter or if the student has already used part of that timeline.

- The student must remain continuously enrolled in the same program of study at the same institution as they were enrolled as of June 30, 2026,

AND meet ONE of the following:

- The parent borrower must have had a Parent PLUS Loan disbursed for that same program before July 1, 2026, OR

- The student must have had a Direct Loan (subsidized or unsubsidized) disbursed for that same program before July 1, 2026.

Continuously enrolled means the student is not withdrawn from all courses or otherwise cease enrollment outside of scheduled breaks or non-required terms, such as summer).

New Graduate Unsubsidized Loan Limits Annual Limit: $20,500

Aggregate Limit: $138,500

Annual Limit: $20,500 (unchanged)

New Aggregate Limit $100,000 (only graduate Unsub loans)

New Lifetime Limit:

$257,500 (combined Sub/Unsub as Undergraduate and Grad, including Grad PLUS)

Aggregate & Lifetime Limit Exceptions:

The law allows some students to be exempt from the new Direct Unsubsidized aggregate and lifetime borrowing limits under a limited exception through their time to completion, for a maximum of 3 years. Students may qualify for the limited exception if:

- They remain continuously enrolled in the same program of study at the same institution as they were enrolled as of June 30, 2026

AND

• They had a Direct Loan disbursed (Direct Unsubsidized or Graduate PLUS) for that same program before July 1, 2026 - What happens when students no longer qualify for the Parent PLUS Legacy exception?

-

After three academic years, or earlier if the student withdraws or otherwise ceases enrollment from their current school or completes their program of study, Parent PLUS Loan borrowers become subject to the new $20,000 annual and $65,000 aggregate loan limits.

- What if a Parent PLUS Loan borrower needs more than the annual borrowing limit, or reaches the aggregate limit before the student graduates?

-

Reach out to the One Stop Delhi Student Services Office about other financing options, like campus based or external scholarships, payment plans, or private student loans.

- Can a NEW student’s parent get a Parent PLUS Loan for 2026–27 under the time‑limited Legacy exception if they apply before July 1, 2026?

-

No. Students accepted for Fall 2026 or later are subject to the new borrowing limits.

- Does changing majors disqualify Parent PLUS borrowing under the Legacy exception?

-

We are waiting on further clairifcation on this topic and the information below was obtained from the National Association of Student Financial Aid Administrators (NASFAA), which is subject to change.

No, as long as the student remains within the same program of study and same degree type at the same institution.

Example 1: The student changes from an Accounting major to a Business major at the same school. Both are Bachelor of Business Administration (BBA) degree programs, so the student has changed from one BBA program to another BBA program. This student stays within the bachelor's degree type, so they can change majors and are still enrolled in the same program of study for purposes of qualifying for the parent PLUS legacy limits.

Example 2: The student changes from the Veterinary Technology major (which is a BS degree) to the Healthcare Management major (which is a BBA degree) at the same school. This student stays within the bachelor's degree type (BS to BBA), so they can change majors and are still enrolled in the same program of study for purposes of qualifying for the parent PLUS legacy limits.

Example 3: The student changes from an associate's degree to a bachelor's degree at the same school. This student does not stay within the same degree type, so they have changed program of study and no longer qualify for the parent PLUS legacy limits.

The same applies if the student transfers from a bachelor’s degree to a master's degree.

Example 4 (Transfer Students): The student transfers from a BBA in Accounting from a college in NYC into a BBA in Accounting at SUNY Delhi. While this student stays within the same degree type, they are not enrolled in the same program of study at the same school and no longer qualify for the parent PLUS legacy limits.

- What does the expected time to credential mean and how do I calculate it for the Legacy exception?

-

The Expected Time to Credential is the published length of your program by SUNY Delhi. For example, an associate's degree is 2 years and a bachelor’s degree is 4 years.

For students who were enrolled in Spring 2026, starting July 1, 2026, the legacy exception looks at how long the student is expected to need to finish their program. This expected time is whichever of the following is shorter:

- Three academic years (as defined in federal regulations), OR

- The time left in the student’s specific program, which is calculated by taking:

- the full length of the published program, minus

- the part of the program the student has already completed as of the date you make the determination.

Example:

The student is in a bachelor’s program that has a published program length of 4 years.

The student completes their first year at the end of 2025-26 and is scheduled to return for their second year in 2026-27.

According to the program length, they should be enrolled:

- 2025-26 – Year 1

- 2026-27 – Year 2

- 2027-28 – Year 3

- 2028-29 – Year 4 (graduates)

The student's parents borrowed $20,000 in parent PLUS funds for the 2025-26 academic year.

Q1) Can the parent borrow under the legacy limits?

A1) Yes. The student’s parents would qualify for a PLUS loan under the interim exception.

This is because the student’s expected time to complete the credential is the lesser of:- Three years, or

- The remaining length of the program, calculated as:

- Total program length: 4 years

- Time already completed: 1 year

- Time remaining: 4 − 1 = 3 years

Since the remaining program length is 3 years, the borrower has 3 years of eligibility under the interim exception.

Q2) When would the parent no longer be eligible for the legacy limit?

A2) After the 2028-29 academic year. If this borrower enrolled in 2029-30, the interim exception would have expired and they would no longer be eligible for the exception. Additionally, this student would lose interim exception eligibility earlier if they withdrew or otherwise ceased to be enrolled in the program of study at any point after receiving the interim exception.

Q3) If the parents borrowed at least $65,000 aggregate in parent PLUS when the student reaches the period where they lose interim exception eligibility, what is the student’s eligibility for parent PLUS funds when the student returns to school at that time?

A3) During the student’s expected time to credential, the parents are not subject to the aggregate loan limit of $65,000; however, when the exception expires, the limit kicks in and looks at all that has been borrowed. If the parents borrowed at least $65,000 on the student’s behalf, they have exhausted their eligibility.

Academic Year

Period Enrolled

Interim Exception Status

2025-26

Year 1

N/A

2026-27

Year 2

Interim Exception Year 1

2027-28

Year 3

Interim Exception Year 2

2028-29

Year 4

Interim Exception Year 3

2029-30

Year 5 (if enrolled)

Exception expired – new loan limits apply

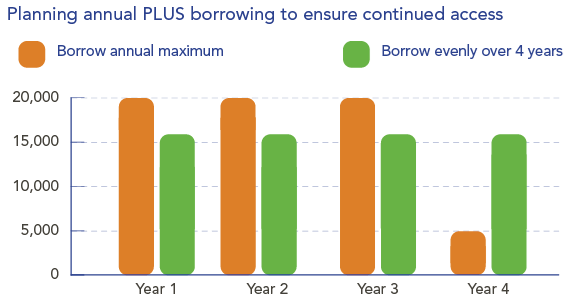

- How much should a parent borrow in a Parent PLUS loan under the new regulations?

-

On the Parent PLUS Loan application, parents should only select the “maximum amount” option if they wish to borrow the full $20,000 for the year.

To ensure adequate Parent PLUS Loan eligibility for the duration of the student’s undergraduate program, parents may request a lesser amount on the application.

For example, request $16,250 per year for total (aggregate) eligibility to be split equally for a four-year program.

- What is NOT impacted by the new loan limit regulations?

-

The annual and aggregate loan limits for an undergraduate student (2, 4 and 5 year programs) are not changing. The only part that is changing is if attending part-time, the loans are subject to the new Schedule of Reduction (SOR).

The annual loan limit for Graduate Unsubsidized loans is not changing. The only changes includes new limits to the aggregate and (new) lifetime limits, as well as being subject to the new part-time schedule of reduction.

Students may still qualify for loan forgiveness (through PSLF) under the new repayment program for subsidized and unsubsidized loans only.

Q&A: PARENT PLUS REPAYMENT/FORGIVNESS

- I'm a parent PLUS borrower and my loan(s) first disbursed before 7/1/2026, and I don't plan to borrow a new parent PLUS loan on or after 7/1/2026

-

Under the new law, repayment options for Direct Parent PLUS loans will be restricted. If you have Direct Parent PLUS loans and do not plan to take out additional federal student loans, taking action now is essential to preserve access to income-driven repayment plans and loan forgiveness, include Public Service Loan Forgiveness (PSLF).

Time is limited to complete the necessary steps to preserve your payment plan and forgivness options. Parents that need assistance should reach out to NYS EDCAP for free loan counseling. This service is only available to NYS residents.

Additional information can be found on the OBBBA update webpage.

- I'm a parent PLUS borrower, and all of my loans are disbursed before 7/1/26, and I do plan to borrow new loans on or after 7/1/26

-

1. If you have parent PLUS loans or a Direct Consolidation Loan that includes a parent PLUS loan, or any other type of Direct Loan, any of which are first disbursed on or after July 1, 2026, then you’re permitted to repay the Direct Consolidation Loan or the parent PLUS loan under only the Tiered Standard Plan.

2. If you have other types of Direct Loans that are not a PLUS loan for parents or a Direct Consolidation Loan that includes a PLUS loan for parents, then those other loans may be repaid under either the Repayment Assistance Plan or the Tiered Standard Plan.

3. If you have a Direct Consolidation Loan that paid off a Direct Consolidation Loan that paid off a PLUS loan for parents (sometimes referred to as a double consolidation) or any other type of Direct Loan, any of which is first disbursed on or after July 1, 2026, then you’ll have access to only the Tiered Standard Plan for your Direct Consolidation Loan or your parent PLUS loans.

Public Service Loan Forgivness (PSLF)

The Tiered Standard Plan doesn’t count as qualifying payment toward PSLF or Temporary Expanded Public Service Loan Forgiveness (TEPSLF).

Some exceptions may apply to qualify for TEPSLF. Visit the OBBBA update webpage for more information.

All information above is subject to change.

Fall 2026 New Student Finanical Aid Offers

New students that have been accepted for Fall 2026 and have completed the 2026-2027 FAFSA will start to receive their financial aid offer via their SUNY Delhi email, FAFSA student email, and SMS (if opted-in) as early as December 2025. Students can still apply for financial aid by starting with the FAFSA application at studentaid.gov/fafsa.

Fall 2026 NYS Excelsior Tuition Scholarship Application

Students from families earning $125,000 or less could receive a scholarship to cover up to the cost of their tuition, after other grants and scholarships are applied first. The Fall 2026 application deadline is August 31, 2026 for new applicants.

Visit the Excelsior Scholarship webpage for more eligibility information and to apply. Returning recipients do not need to reapply for Excelsior but must submit the annual FAFSA and TAP application. This scholarship will not cover other costs such as room, meals, or fees.

Consent to Release Financial Aid & Billing Information

Individuals calling on behalf of the student must be authorized to discuss specific financial aid and billing account information.

Students may submit an online Financial Aid and Billing Consent to Release Information form at any time to authorize the offices of Student Financial Services and the One-Stop Delhi Student Services speak with individuals such as parents, guardians, relatives, counselors, employers etc.

Visit our Forms webpage for instructions.

Important Updates Regarding Summer Pell Grant Eligibility

Students who are eligible for the Pell Grant should enroll in all summer courses before the Pell Recalculation Date (PRD). The PRD is a point in time when the Pell Grant will not adjust (up or down) based on changes made to a student’s schedule. Policy updates regarding Pell Recalculation Dates (PRD) can be found on the Important Policies webpage.